September seems to be very crucial month for every Company. In the month of September, many compliances, especially compliances related to preparation and reporting of Financial Statements are due like Income Tax Return are to be filed, Financial statement and Directors report needs to be finalised, Annual General Meeting is to be conducted, ROC reporting is to be processed.

Hence, lot of pressure and burden is on the Company as well as for the Professional. An effort has been made to explain in a simplified manner the process of annual filing in case of a private limited company for better understanding of the stakeholders.

Preparation of Financial Statement

The financial statement so prepared shall depict the performance of the company during the financial year.But, before moving forward, we should know what is the meaning of Financial Year.

Financial Year

Pursuant to Section 2(41) of the Companies Act, 2013, Financial year means the period ending on the 31st day of March every year, and where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year. Every Company after ending of Financial Year,is required to report to the Registrar of Companies its financial statement as well as the Annual Return.

The financial year for the purpose of Income Tax is defined as the period starting from the date of incorporation or the 1st day of April of the year and ending on the upcoming 31stday of March.Infact, the reporting is to be done even for one day, irrespective of profit earned or not, transaction entered or not.

Financial Statement:

Section 2 sub section 40 of the Companies Act, 2013 defines “financial statement” in relation to a company, includes—

(i) Balance Sheet: basically, a statement which shows the position of a Company as on the last date of the financial year

(ii) Profit and Loss Accountor an Income and Expenditure Account: Statement that reflect the transactions entered during the financial year with respect to income earned and expenses incurred;

(iii) Cash Flow Statement: Statement showing inflow and outflow of funds for the financial year;

(iv) a statement of changes in equity, if applicable; and

(v) any explanatory note annexed to, or forming part of, any document referred to in sub-clause (i) to sub-clause (iv):

Provided that the financial statement, with small company may not include the cash flow statement.

Reporting

- Reporting to Income Tax

Every Company has to report details of its financial statement and profit and loss account with the Income Tax Department. Further, tax needs to be paid in case of any profit is earned after deducting all the relevant expenses.

Tax rate on Companies are as follows:

- – Turnover exceeding Rs. 250 Crores: 30%

- – Turnover below Rs. 250 Crores: 25%

Though the financial statement are prepared as per Companies Act, 2013 but the Tax Return is to be filed only after considering the Income and Expenses allowed under the Act and the rate of depreciation as prescribed therein.

Last date for filing of Income Tax Return along with tax audit report is the30th day of the September of the assessment year.

Wherein the Assessment Year means the period of twelve months commencing on the 1st day of April every year immediately after the closure of Financial Year.

- Reporting to Registrar of Companies

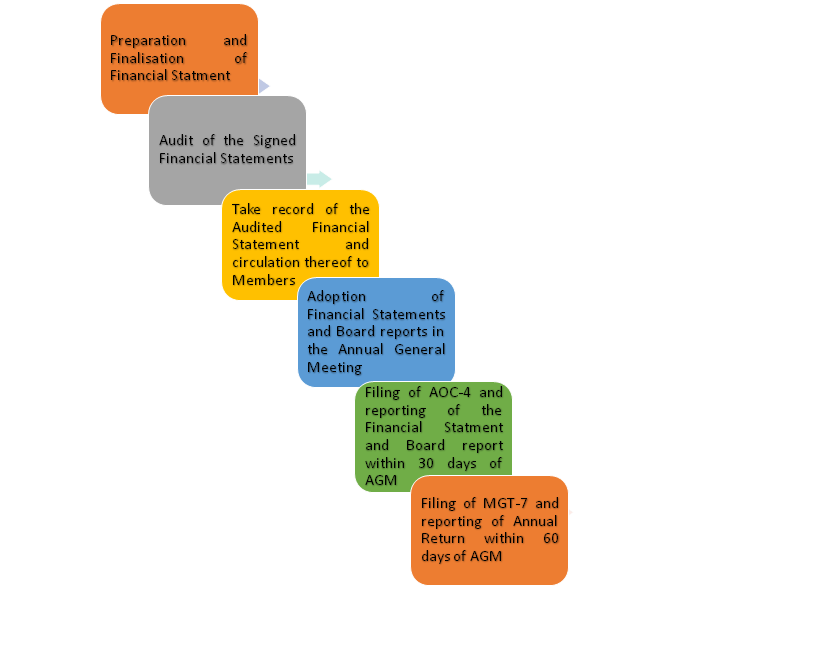

The reporting of the Registrar of Companies starts with preparation of Financial Statement. The financial statement shall contain monetary details of all the transaction entered during the financial year. Once the financial statements are prepared, the same is to be presented before the Board. The Board shall approve the Financial Statements and forward the same to the Statutory Auditor of the Company. Once the audited financial statements are received, the same shall be circulated along with the Directors Report among the Members. The Financial Statement and the Directors Report shared shall be presented before the Members in the Annual General Meeting for adoption. Once the approval is received, the same are adopted, and are required to be reported to the Registrar of Companies in the following forms:

| Sl. No. | E-Forms | Purpose of the Form | Due Date |

| 1. | AOC-4 | Reporting of Financial Statement | 30 days from the date of AGM |

| 2. | MGT-7 | Filing of Annual Return | 60 days from the date of AGM |

| 3. | ADT-1 | Appointment of Statutory Auditor | 15 days from the date of AGM (to be filed only if applicable) |

| 4. | DIR-12 | Filing of change in Designation of Directors | 30 days from the date of AGM (to be filed only if applicable) |

Fine and Penalties

Delay in filing of Form AOC-4 and MGT-7 would attract additional fee of Rs. 100/- (Rupees One Hundred only) per day per form. Hence, forms to be filed within due time is highly commended.

Compliances are not expensive only if completed before time instead of waiting for last minute rush.

Conclusion

The procedure for preparation and filing of Forms has been presented in a simplified manner for better understanding. In case of any issue, visit our website at www.complianceship.comor you can also mail us at contact@complianceship.com and even drop us a whatsapp @ +91 8010233173

Leave a reply